Table of contents

Open banking payments are A2A (account-to-account) or Pay by bank app payments, where the payment moves directly from the payer’s bank to a merchant’s bank.

Open banking is a secure way for consumers to give merchants or service providers access to their financial information or to authorise a payment directly from their bank account, usually via payment processing companies like Wonderful.

How exactly do Open Banking payments work?

- Open banking depends on APIs (application programming interfaces). APIs enable software to speak to other software.

- APIs are effectively the instructions on how a third party can access data from a bank (account holder’s name, account type, currency, personal details).

- Open banking payments are completed securely and only with the sender’s consent.

Tell me why I should use open banking payments?

The growing digitalisation of payments has been driven further by the coronavirus pandemic, with 52% of payments made via card. The increase in maximum transactions for contactless payments has also steered society towards the convenience of digital payments. Open banking doubles down on this convenience by going above and beyond through:

- Simplicity: Consumers only have to authenticate themselves once to give permission to an Open Banking payment initiation service, then they can easily pay directly from their bank account every time, without having to enter card details or enter further credentials.

- Speed: Open banking enables instant bank payments , allowing funds to be transferred immediately.

- Trust: Customers feel more secure when they can select a familiar, trusted route to make a payment. There’s nothing more familiar for most than using their own bank account and their usual bank login.

|

Open Banking payments |

Card payments |

|

|

Cost to merchant* |

From 4p / transaction |

From 1.4℅ +20p / transaction |

|

Settlement speed |

Instant via Faster Payments |

1-3 days |

|

User experience |

Good. Automated, mobile first, made for digital, integrated into checkout. |

Good when websites store information, otherwise manual data entry required. |

Are open banking payments safe?

Bank-level security – Open banking uses rigorously tested software and security systems. You’ll never be asked to give access to your bank login details or password to anyone other than your own bank or building society.

It’s a regulated pay online system – only apps and websites regulated by the FCA or European equivalent can enroll in the Open Banking Directory.

You’re in charge – you choose when, and for how long, you give access to your data.

Extra protection – your bank or building society will pay your money back if fraudulent payments are made. You’re also protected by data protection laws and the Financial Ombudsman Service.

How is open banking influencing the digital payments transformation?

Card payments, direct debits, and wire transfers have existed for decades. While they still play an important role in the financial sector, open banking has tapped into hitherto unexplored possibilities. By enabling third-party providers to access bank data in a secure and seamless manner, open banking is fostering remarkable innovation, healthy competition, and services that truly prioritise the needs of customers. Businesses, financial institutions, and consumers are experiencing the advantages of quicker transactions, improved security, and tailored financial products, all while minimising the challenges usually linked with traditional banking. Let’s take a closer look at how open banking is shaping the future of monetary transactions:

FinTech integration

Financial services and FinTech companies can easily interact with banking systems via open banking APIs, generating more innovative and user-friendly online payment solutions. This makes way for a more collaborative ecosystem that helps businesses and consumers.

Cost optimisation for businesses

Open banking payments are a more cost-effective alternative for businesses, particularly those with high transaction volumes, as they eliminate the need for traditional payment intermediaries, thereby reducing transaction fees.

Personalised financial solutions

With insightful analytics at your fingertips, you can offer your customers tailored financial solutions that meet their specific requirements.

Encouraging healthy competition

Open banking removes entry barriers, thus allowing smaller banking and non-banking financial institutions to compete with their larger counterparts. Now that fintech companies may compete with more established financial institutions, customers have additional payment options to choose from.

Promoting digital-first banking

The emergence of digital-only banks is inextricably linked to open banking, as these institutions rely on open APIs to offer their consumers seamless payment and banking services without the necessity of physical branches.

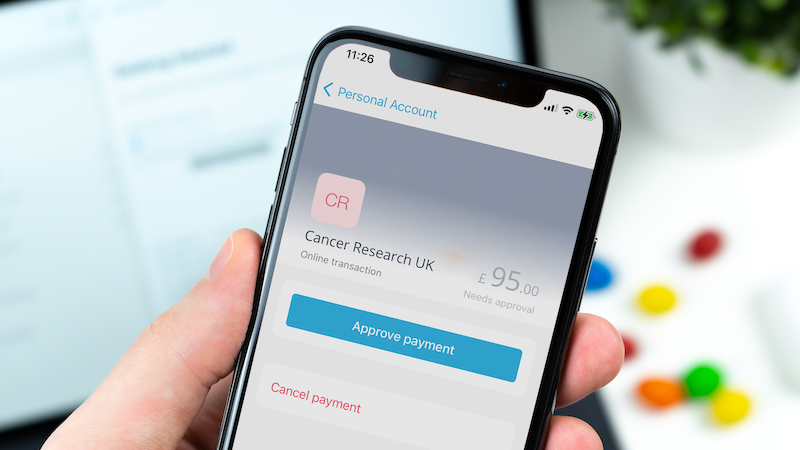

Why should charities use open banking payments for donations?

Convenience – The fast nature of open banking instant payments means that donating is more convenient and easier to complete. This promotes donating as it is hassle-free. The knock-on effect from this is a greater likelihood of donations.

Covid-19 – With the recent requirements of social distancing, there has been a natural drop in the number of in-person donations. open banking’s ease-of-use makes this the best and most suitable alternative payment method.

Zero Transaction Fees – Card payments are accompanied by processing fees. open banking payments are A2A (Account to Account) transfers, which removes these fees altogether. This means that the value of donations are higher, and you can maximise your fundraising because of this.

Security – The safety that open banking offers builds greater trust in charities from donors. Charities not handling any financial data (because of A2A) reassures donors that their money and information is safe. This greater trust and display of ethics will likely encourage donations.

What do commercial businesses gain?

- Competition – Increased competition leads to greater innovation in financial products. If one retail company utilises open banking and another competitor does not, this creates opportunities to develop.

- Products - With the sharing of information becoming encouraged, banking data through open banking Payments can be utilised to create new financial products. These include funding platforms, supplier payment, services, credit checks, and insurance. These can then be competitively priced to suit customer need.

- Speed – Having access to an individual’s or company’s financial data should greatly reduce the time it takes for financial services to be set-up; for example, providers may be able to approve loans much more quickly. Retailers could also process payments much faster, meaning access to the product or service being paid for may be faster too.

- Improvement - With information now more available than ever before, we might see other industries looking to utilise this data to improve their services and offerings for clients. For example, in recent years, the introductions of APIs changed the face of the travel sector.

How is the use of open banking payments adopted?

In 2016, The Competition and Markets Authority (CMA) found that older, larger banks don’t have to compete hard enough to gain customers’ business, while newer banks find it difficult to access the market and grow.

One of the CMA’s recommendations to tackle this problem was open banking. This means that open banking is more commonly used by newer banks to offer better competition to traditional, more established banks. Examples of these include Monzo and Starling Bank.

Examples

Buy now, pay later - “Buy now, pay later”, has become the new trend of the pandemic times. Its main priority is to ensure the highest purchase conversion rates possible, by providing customers with extra short term and interest free purchase options. The newest trend in online shopping is essentially a financing arrangement that allows customers to make purchases without the need to pay the product's full price all at once. Even though it may sound like traditional credits, with BNPL customers are offered options that split the price into a few instalments, often interest-free.

With the integration of open banking on BNPL, providers can further improve their approval rates and provide better assessment for their customers. Without the need to connect with traditional credit bureaus and the possibility to make quick analysis of current financial data, providers assure that every assessment takes into consideration the current financial situation and habits of the customer.

Insurance companies can offer tailored packages - the arrival of open banking means that players in this market can take advantage of new tools.

There are multiple insurance quote comparison platforms online, that constantly help customers to find the perfect match for their needs. Now, with the implementation of open banking in their platforms, they can provide a more accurate assessment to each person individually taking in consideration the cash flow on their bank accounts, current loans, etc.

Crypto can tackle the challenge of smooth connections between wallets and bank accounts - One of the challenges in the crypto exchange market is how platforms can assure customer safety, smooth and fast user experience when buying, selling and trading assets. Open banking can present itself as the solution, allowing for a frictionless customer experience when dealing with funds, as well as faster identity verification.

Open banking: expanding beyond the United Kingdom

Open banking is no longer a UK-centric phenomenon; its global acceptance has spread far and wide, impacting online payment systems around the world.

PSD2 regulation (Payment Services Directive 2) has been the primary driver of open banking in the European Union, requiring banks to disclose their payment and consumer data to third-party providers. This has expedited the adoption of open banking throughout Europe, resulting in improved financial services and payment options for both consumers and businesses.

Open banking is also acquiring traction in countries such as Australia as a result of the Consumer Data Right (CDR) legislation, which grants consumers more control over their financial data. The CDR facilitates a more competitive financial landscape by enabling individuals to share their banking information with trusted third parties securely. This is opening the market for more customised payment solutions that cater to a larger consumer base with varied preferences.

While Asia, particularly Singapore and India, are emerging as hubs for open banking, the US is still playing catch-up with its nuanced regulatory framework. Despite the challenges, financial institutions and fintech companies in the United States are boldly adopting open banking models. Services such as Plaid are paving the way for open banking payment integrations, inspiring banks and non-bank financial institutions to explore ways to embrace similar technologies.

As the global financial ecosystem evolves, opportunities for collaboration between regions emerge, paving the way for a more unified and accessible global open banking system.

Industrial applications of open banking

Real-time payments, a secure transaction platform, and cost-effectiveness are key drivers of the rapid adoption of open banking across various sectors. Open banking's flexible payment model makes it adaptable to different industrial needs, extending its scope from retail to healthcare and beyond. Let’s look at its impact across various industries:

E-commerce and retail

Open banking facilitates faster checkouts and eliminates the necessity for card details, thereby improving the purchasing experience and decreasing cart abandonment rates for online retailers.

Healthcare

Healthcare providers benefit from quicker fund settlements and simpler payment reconciliation. For expenses outside their insurance coverage, patients can make instant payments for services or prescriptions directly from their bank accounts.

Hospitality and travel

The hospitality and travel sectors, including hotels and airlines, can leverage open banking to optimise booking payments, expedite refunds, and simplify the administration of recurring charges, such as membership or loyalty program fees.

Education

The edutech industry is one of the primary adopters of open banking. Educational organisations, such as universities and online learning platforms, can utilise various subscription management tools to automate tuition and subscription payments for courses, enhancing cash flow and simplifying fee management for both students and administrators.

Photo by Jannis Lucas on Unsplash